Taxes During Home Foreclosure: Capital Gains and Income Due to Debt Cancellation

Losing a home or any other property through foreclosure can be personally and financially devastating, and to rub salt into the wound, it can also lead to a tax liability. If your property is foreclosed on, you may face:

- Capital gains – The tax code treats a foreclosure as if you sold the property.

- Cancellation of debt (COD) income – Canceled loans are generally treated as income. That rule applies to recourse mortgages but not to non-recourse mortgages.

Let’s look at both of these federal tax implications in the event of a foreclosure, but first, we need to explain the difference between recourse and non-recourse loans.

Recourse Vs. Non-Recourse Mortgages

The tax treatment of a foreclosure varies depending on whether the loan is a recourse or non-recourse loan:

- Recourse loan – The borrower is personally liable for the loan. If the underlying collateral is not enough to cover the loan, the lender can go after the borrower's other assets.

- Nonrecourse – The borrower is not personally liable for the loan. The lender can only take the collateral to satisfy the loan.

State laws, the type of loan (purchase or refinance), and what the note actually says determine whether the loan is recourse or non-recourse. The type of loan affects how you calculate the capital gain or loss, and it also determines whether or not there is any cancellation of income.

Capital Gain or Loss After Foreclosure

To calculate capital gain or loss, subtract the property's basis from the amount realized. Usually, that's the sale price, but in a foreclosure, it's either the property's fair market value or the value of the outstanding loan, as explained below.

If the loan is classified as a recourse loan, the amount realized is the lower of:

- The property's fair market value, or

- The outstanding liability before the foreclosure.

If the loan is a non-recourse loan, the amount realized is:

- The outstanding liability right before the foreclosure.

To illustrate, let's say that Mike buys a home for $700,000. That's his basis in the home. A few years later, he can no longer make payments, but he still owes $650,000 to the bank. But due to declining property values, the home's fair market value is only $500,000.

To calculate the capital gain or loss on a recourse loan, he starts with the lower of the home's fair market value or the amount owed on the loan. In this case, the lower amount is the FMV at $500,000. When you subtract his basis, he has a capital loss of $200,000.

In contrast, if he had a non-recourse loan, he would calculate the capital gain/loss by subtracting his basis ($700,000) from the amount owed to the bank ($650,000), making the loss $50,000.

Do I owe taxes if there is a capital gain with the foreclosure?

It depends. If the gain was on your home, you qualify for a capital gains exemption of $250,000 for an individual or $500,000 for a married couple filing jointly. To qualify, the home must be your primary residence that you have lived in for at least two of the last five years.

If the property was not your primary residence or if the gain exceeds the primary residence threshold, report the gain on Schedule D. If the foreclosure was business property, report it on Form 4797.

Can I write off a capital loss due to foreclosure?

Unfortunately, you can never claim a loss from the sale of your home – that's considered to be personal property. If you have a loss due to selling business property, you can use that to reduce other business or investment income, and up to $3000 of wages.

Cancellation of Debt Income

In addition to incurring capital gains during a foreclosure, you could also face taxes on canceled or forgiven debt. This only applies if the lender forgives the debt on a recourse loan – it does not apply if the lender rolls the balance due into an unsecured loan. There's also no income to report if the forgiven loan was a non-recourse loan.

Most home loans are recourse loans, and in fact, only 12 states allow lenders to use non-recourse loans for home mortgages.

To calculate the cancellation of debt income, subtract the FMV of the property from the amount of the outstanding debt right before the foreclosure.

To continue with the above example, Mike owes $650,000 to the bank, and the FMV of his home is $500,000. He has $150,000 in cancellation of debt income. However, if he had a non-recourse loan, he would not have any income due to the canceled debt.

Exceptions to Owing Taxes on Forgiven Liabilities With Recourse Loans

Even with a recourse loan, you may not face taxes on forgiven loans if you qualify for one of these exceptions:

- Insolvency – If your loans exceed the fair market value of your assets when the loan is forgiven/ canceled, all or part of the forgiven amount may not cause tax liabilities.

- Bankruptcy – Liabilities canceled or discharged in bankruptcy are generally not taxable.

- Intended as a Gift – If the cancellation is intended as a gift, you may not have to report the cancellation of liability income.

Do I have to report income from the cancellation of debt on my primary residence?

Through tax year 2025, you can exclude up to $2 million in forgiven mortgage debt for married couples filing jointly. This was originally a provision of the Mortgage Forgiveness Debt Relief Act of 2007. It has expired and been extended many times since then, and most recently, it was extended by the Consolidated Appropriations Act for tax years 2021 to 2025.

Where should I report cancellation of debt income on my tax return?

Report cancellation of debt income for your personal residence on line 8c of Schedule 1 of Form 1040. Or if dealing with business property, report on the appropriate schedule:

- Schedule C (Form 1040), line 6, if the debt is related to a nonfarm sole proprietorship;

- Schedule E (Form 1040), line 3, if the debt is related to nonfarm rental of real property;

- Form 4835, line 6, if the debt is related to a farm rental activity for which you use Form 4835 to report farm rental income based on crops or livestock produced by a tenant; or

- Schedule F (Form 1040), line 8, if the debt is farm debt and you are a farmer.

How much should I report in canceled income?

You should receive Form 1099-C from the lender showing how much debt was canceled. If the bank did not issue a 1099-C, you are still responsible for reporting the canceled debt as income, unless you meet one of the exceptions noted above.

Generally, you report the amount shown in box 2. However, if interest is included in box 2, that will be noted in box 3, and if the interest would have been deductible if paid, you don't have to include that portion in your income. Additionally, if the property was owned jointly, the lender may issue 1099-C forms to both of you with box 2 showing the total debt canceled – in that case, you should report your share of the income.

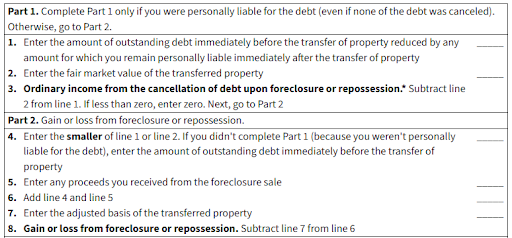

Worksheet to Calculate Forgiven Liability Income & Capital Gains

Want to figure out how much income and/or capital gains you may incur due to foreclosure? Then, use this worksheet from the IRS.

What if the mortgage's remaining balance is converted to a loan?

Lenders may convert the remaining loan amount to an unsecured loan. If this happens, you do not have to report any income related to the canceled debt. But remember, you cannot deduct this interest with your itemized deductions.

What if the IRS seizes my home?

If the IRS seizes your home for unpaid taxes, there may be additional tax consequences. In this situation, there will generally not be any cancelled debt, but there may be a capital gain.

Find Help Using TaxCure

Dealing with a foreclosure of your home or even a business asset can be extremely stressful. Don't let an unexpected tax liability make the process even worse. To get help dealing with capital gains or income due to debt cancellation, contact a tax professional today – using TaxCure, you can narrow down your search to find a local tax pro who can provide you with customized help for your needs.

https://www.irs.gov/faqs/capital-gains-losses-and-sale-of-home

https://www.irs.gov/forms-pubs/about-form-4797

https://www.irs.gov/taxtopics/tc431

https://www.thetaxadviser.com/issues/2022/jul/tax-consequences-real-property-foreclosures/

https://www.irs.gov/help/ita/how-do-i-report-the-debt-forgiven-on-my-residence-due-to-foreclosure-repossession-abandonment-or-because-of-a-loan-modification-or-short-sale